Published December 1, 2025, 1:19 P.M

Discover how Principal & Interest (P&I) loans reduce debt with every repayment. Flint brokers guide first-time buyers and homeowners through P&I loan structures, equity growth, and long-term mortgage strategies.

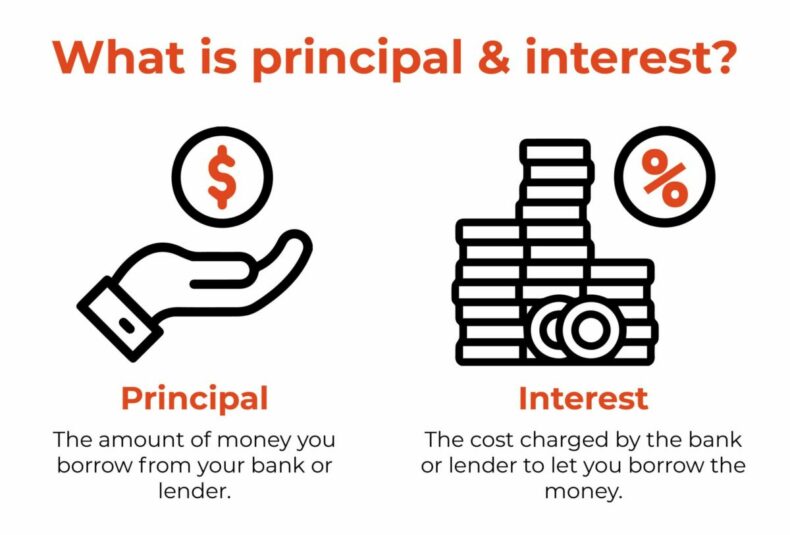

A principal and interest loan is a home loan where each repayment includes:

Over time, your loan balance decreases with every payment, lowering the total interest paid and increasing your equity. P&I loans are a cornerstone of a disciplined mortgage strategy for first home buyers, owner-occupiers, and long-term property investors.

At Flint, we help you:

Chat with Flint today and get a P&I loan strategy that works as hard as you do — one repayment at a time.

Home Loans

Aug 18, 2025

Home Loans

Aug 18, 2025

Home Loans

Aug 18, 2025

Subscribe and be the first to know about what’s happening in the market.

Learn more about how we can help you achieve your financial goals.

Don’t worry, there’s no commitment. Strategic guidance guaranteed.